Wisconsin gives you a head start on college costs. Contribute to Edvest or its advisor-sold sibling, Tomorrow’s Scholar, and up to $5,280 per child drops off your state-taxable income each year—cash back at filing time. After that ceiling, every extra dollar competes nationwide. Several top-ranked 529 plans charge roughly half of Edvest’s fees, add specialty funds Edvest skips, or supply a stable-value sleeve for teens.

This guide spotlights six standouts, explains when to split contributions, quantifies an 18-year fee gap, and maps the article’s flow—deduction check, ranking rules, head-to-head grid, then deep dives. Ready? Let’s make every contribution count.

Weighing Wisconsin’s tax break against lower fees

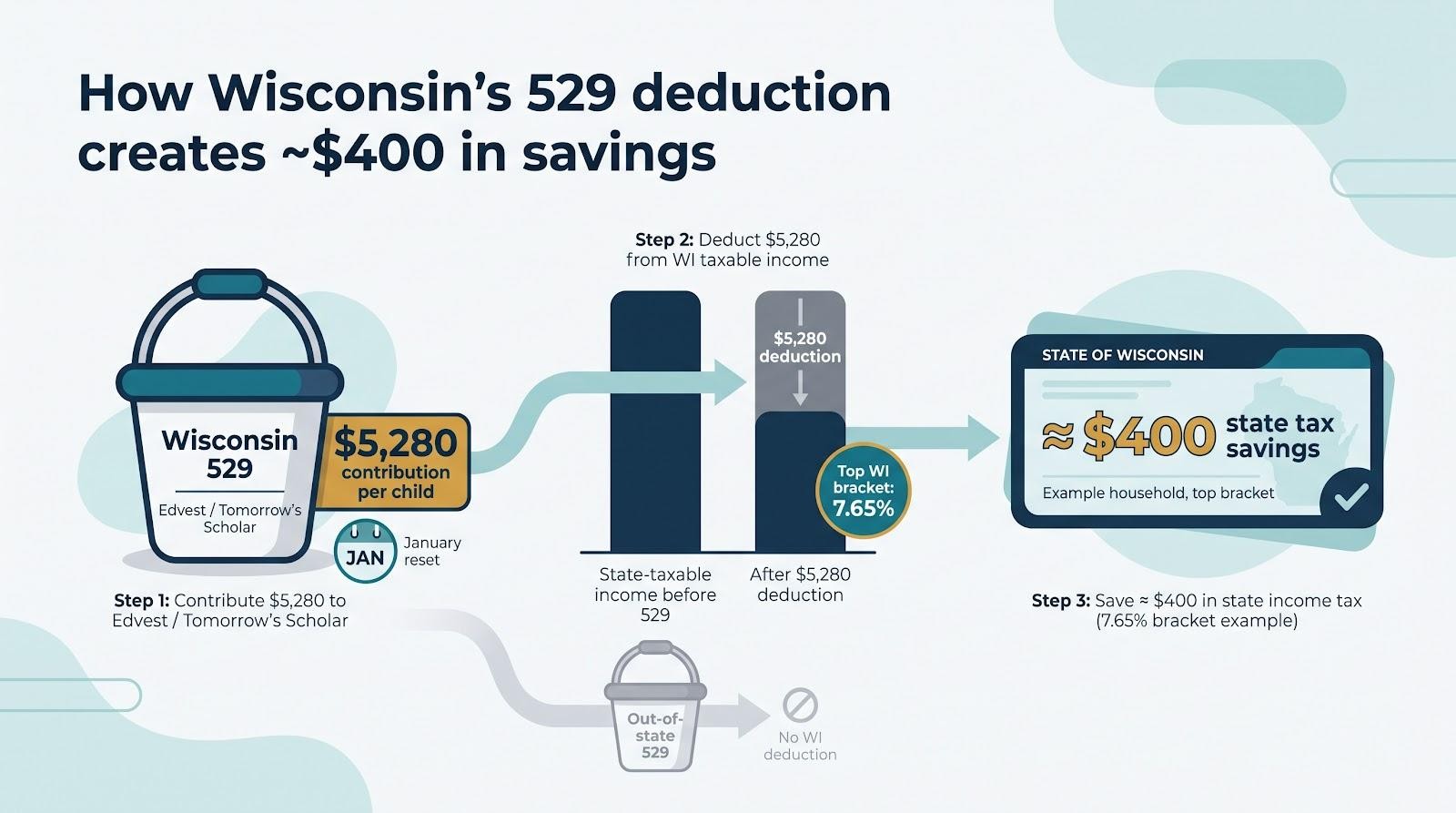

Why the $5,280 deduction deserves respect

Every January, Wisconsin resets the scoreboard. The first $5,280 you put into Edvest or Tomorrow’s Scholar comes straight off your state-taxable income. For a household in the 7.65 percent top bracket, that move locks in roughly $400 of savings. It shows up in your refund the same spring.

Put the same money in another state’s 529 and Madison keeps the tax. Same federal perks, no Wisconsin break. We treat that in-state deduction like an employer 401(k) match and never leave it on the table.

That is why every comparison in this guide starts only after you have maxed the deduction.

When lower fees pull ahead

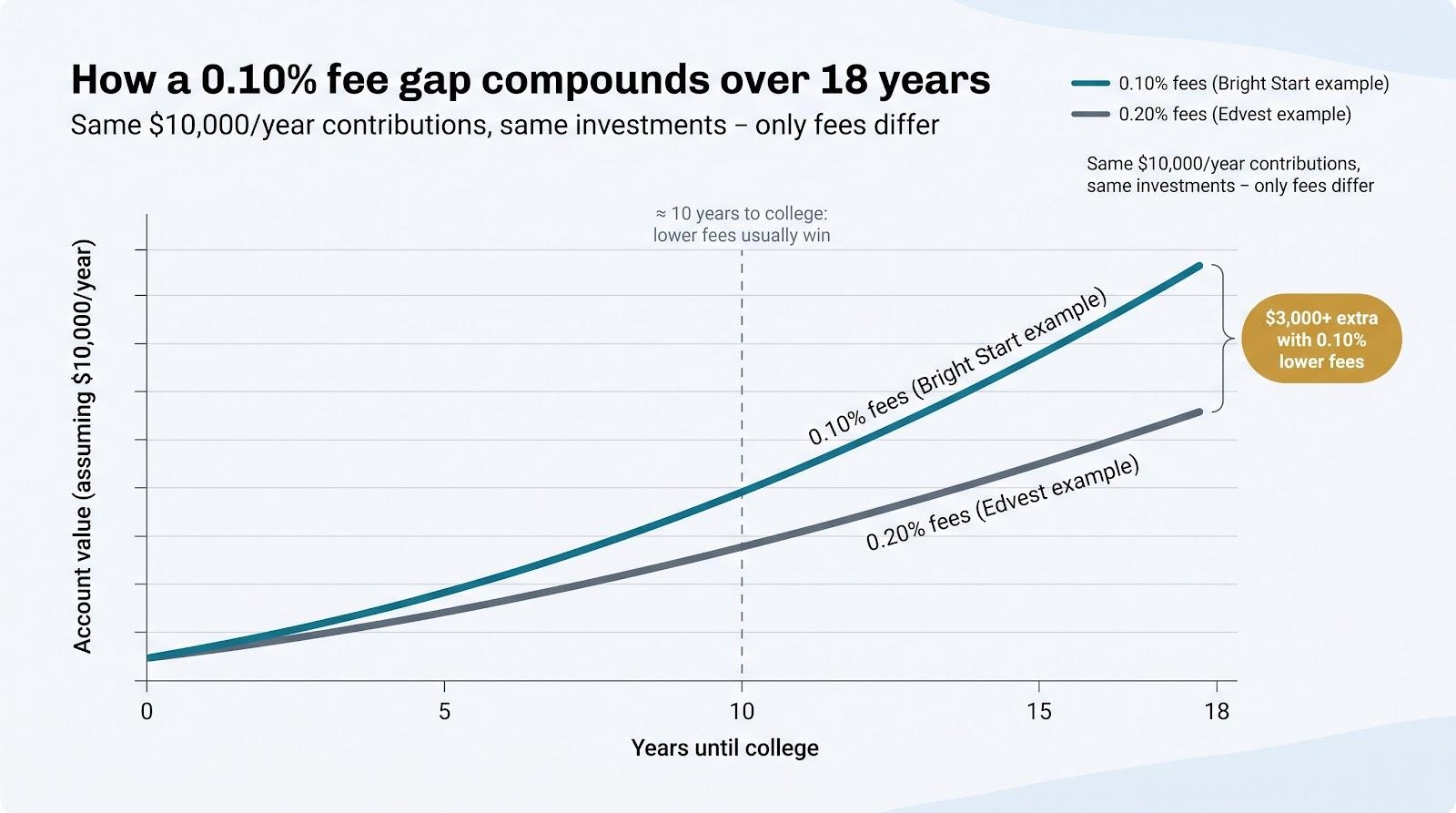

After you claim the deduction, the choice shifts to math. Picture two newborn accounts with identical investments: one in Edvest at a 0.20 percent expense ratio, the other in Illinois Bright Start at 0.10 percent.

That one-tenth of one percent looks small, yet over eighteen years of steady $10,000 contributions, it can add more than $3,000 of extra growth—nearly a decade of Wisconsin tax breaks.

So the rule is simple: if the fee gap is at least 0.10 percent and your child has ten or more years before freshman year, a low-fee out-of-state plan usually outruns the lost deduction. For teens with only a few years left, today’s tax savings win.

Mark Kantrowitz, the long-time 529 analyst behind SavingForCollege, frames it this way: lower fees matter most when the child is young; state tax breaks matter more once high school starts. Our math for a Wisconsin newborn backs him up.

In practice, we seldom face a pure either-or choice. We fund Edvest to $5,280, then direct any extra dollars to one of the six plans below. The split captures the $400 tax win while lower fees work quietly on the rest.

How we picked the six standouts

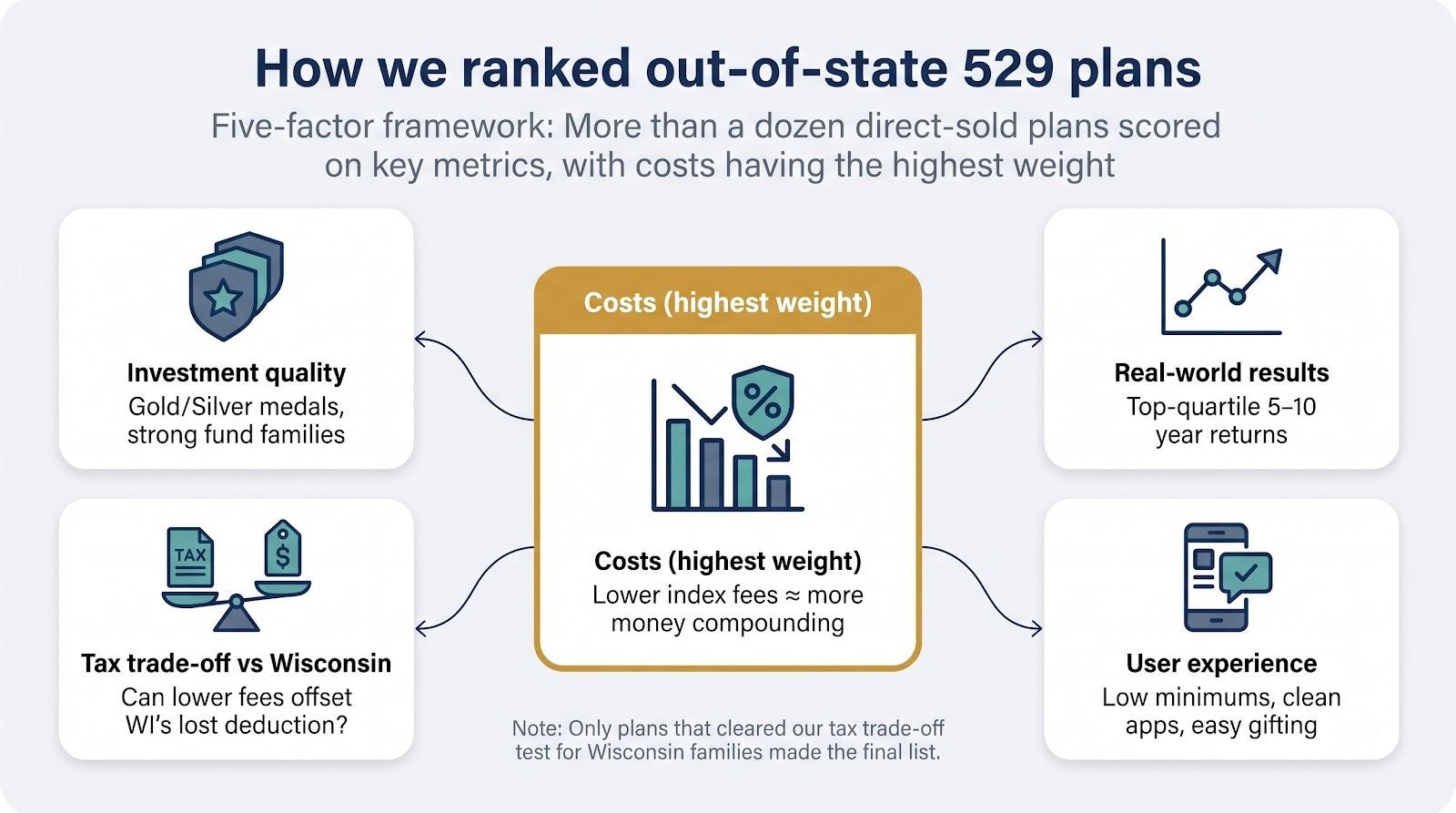

Good rankings start with clear rules. We scored more than a dozen direct-sold 529 plans on five factors that matter once you leave Wisconsin’s tax shelter.

First, costs. Every basis point you pay is a basis point you do not compound, so fees carried the most weight. Plans with index portfolios near 0.10 percent rose to the top, while anything above 0.30 percent stayed off the list.

Second, investment quality. A low fee is useless if the fund menu is weak. We sought Morningstar Gold or Silver medals and broad lineups from names like Vanguard, Fidelity, or Dimensional. Morningstar’s 2025 review supplied the outside seal we wanted.

Third, real-world results. We reviewed five- and ten-year returns on each plan’s age-based tracks. Consistent top-quartile numbers told us the glide paths were working, not just cheap.

Fourth, the tax trade-off. Because Wisconsin gives no deduction on out-of-state plans, we checked whether lower expenses could offset the lost $5,280 write-off over common saving horizons. Only plans that cleared that bar made the cut.

Finally, user experience. Zero-dollar minimums, clean mobile apps, and gifting portals matter when you are juggling baseball practice and bedtime.

Add it up and six plans separated themselves. Next, we stack them up against Edvest so you can see the numbers.

Edvest vs. the leaders: key numbers at a glance

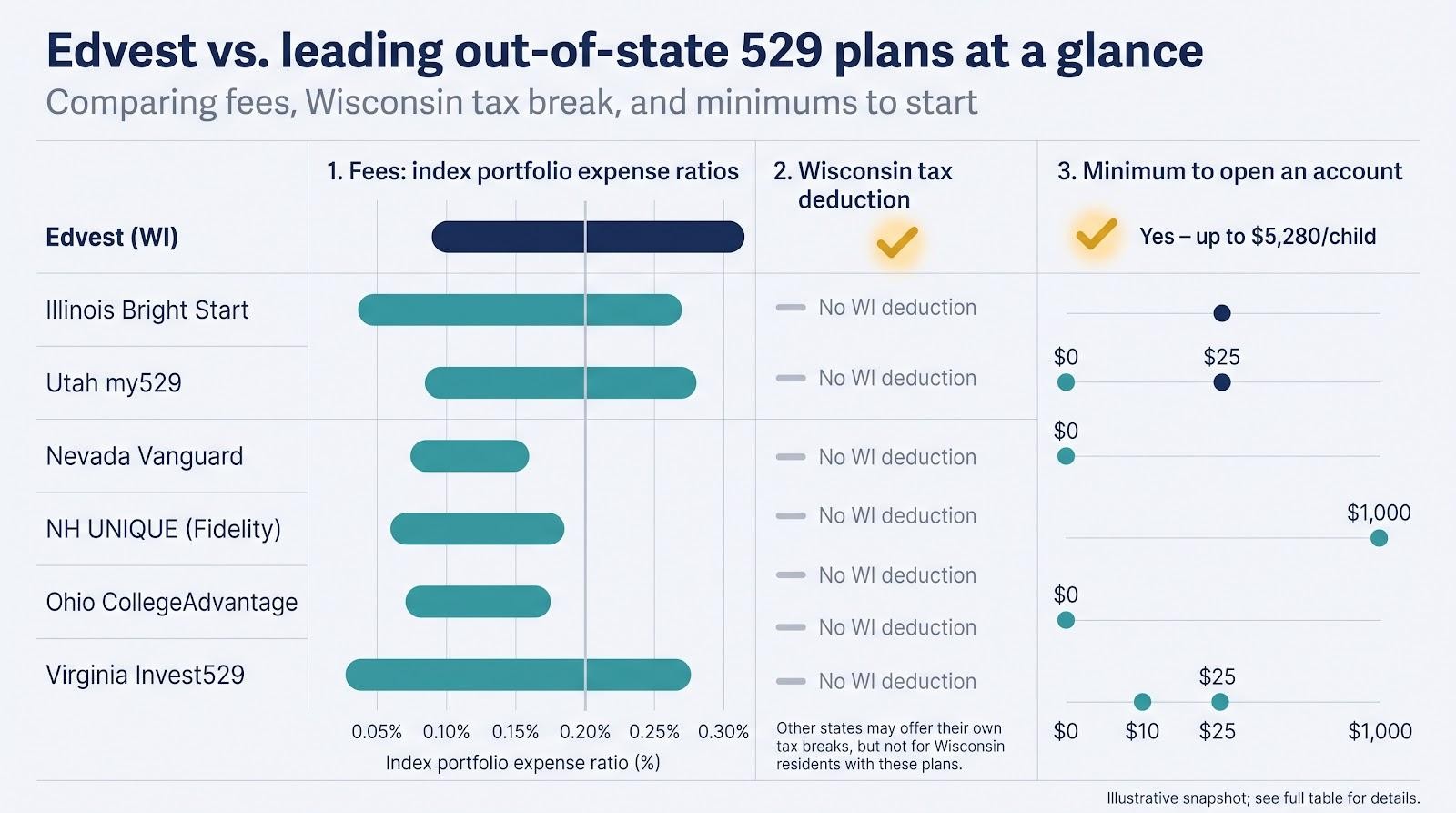

Numbers tell this story quickly. Scan the grid below, then focus on the two or three data points that can guide your next transfer.

| 529 plan | Index-portfolio expense ratio | State tax break | Open to Wisconsinites? | Minimum to start |

| Edvest (WI) | 0.13 – 0.31 % | Up to 5,280 per child deductible on WI return | Yes | $25 |

| Illinois Bright Start | 0.09 – 0.25 % | IL residents get $10k/$20k deduction; none for WI | Yes | $0 |

| Utah my529 | 0.13 – 0.27 % | Small UT credit; none for WI | Yes | $0 |

| Nevada Vanguard | 0.12 – 0.16 % | No state income tax | Yes | $1,000 |

| New Hampshire UNIQUE (Fidelity) | 0.11 – 0.18 % | No state income tax | Yes | $0 |

| Ohio CollegeAdvantage | 0.12 – 0.17 % | OH deduction unlimited; none for WI | Yes | $25 |

| Virginia Invest529 | 0.08 – 0.27 % | VA residents deduct $4,000; none for WI | Yes | $10 |

Three quick takeaways jump off the page.

First, Edvest’s fees land in the middle. Its cheapest index track sits at 0.13 percent, while five of the six outsiders run lower and Virginia reaches 0.08 percent.

Second, only Edvest gives you a Wisconsin tax deduction worth about four hundred dollars a year in the top bracket. Mark the calendar each January to claim it before investing elsewhere.

Third, minimums differ sharply. Nevada needs $1,000 to open an account, a fit for lump-sum savers but tough for new parents. Illinois, Utah, and Fidelity’s UNIQUE plan let you start with pocket change once you pass Edvest’s limit.

Morningstar’s latest medal list backs up the numbers: every plan in the table carries a Gold or Silver rating for process and stewardship. In short, you are comparing high-quality options and choosing the one that fits your budget and style.

Next we zoom into the plans themselves, beginning with the fee leader: Illinois Bright Start.

1. Illinois Bright Start 529: small fees, big lineup

If you want to keep costs as low as possible, Bright Start is the clear choice. Its index portfolios start at 0.09 percent, undercutting Edvest by four basis points and edging past Vanguard’s Nevada plan, and that fee edge carries real weight when average all-in costs at a four-year public university now hover near $31,000 a year—a breakdown explored in How much to save for college. That difference feels tiny until you run the numbers: on steady $10,000 annual contributions over eighteen years, the gap can add more than $3,000 by move-in day.

Illinois Bright Start 529 official homepage screenshot for Wisconsin investors.

Cost savings are only the start. The direct plan offers more than forty portfolios across eleven fund families, so you can stay fully indexed, tilt toward Dimensional factor funds, or mix active managers without opening a new account when your strategy shifts. Morningstar’s analysts call that breadth, combined with firm oversight from the state treasurer’s office, “highly cost-effective,” a verdict that keeps the plan in the Gold tier.

Practical perks seal the deal for Wisconsin parents. There is no minimum to start, no enrolment fee, and the website runs on Ascensus’ clean interface. You can share a one-time gifting link with grandparents in under a minute and watch contributions arrive without writing a check.

The fine print? You give up Illinois’ own tax break, but that was never in play. Bright Start’s role is to boost every dollar after you claim Wisconsin’s $5,280 deduction each year. For most families that second bucket can grow here for decades with minimal attention, delivering the true “set it and forget it” experience a college fund should offer.

2. Utah my529: build-it-yourself flexibility

Utah’s plan is a tinkerer’s playground. Keep its smart age-based tracks or create your own mix from about two dozen Vanguard, Dimensional, and PIMCO funds. Want 70 percent U.S. equity, 20 percent international small-cap value, and 10 percent TIPS? Move the sliders, hit save, and you are done. No other 529 lets you adjust allocations this deeply without an advisor.

Even with that freedom, costs stay slim. Indexed options average 0.13 percent, and an all-index custom portfolio can drop near 0.10 percent. That matches Bright Start and sits well below Edvest’s comparable tracks.

Utah my529 529 plan official website screenshot highlighting customization.

Performance follows the low fees. Morningstar has awarded my529 a Gold rating every year since the medal system launched, praising its thoughtful glide path and steady fee cuts.

Opening the account costs nothing. Fund it with twenty dollars on payday, set a recurring transfer, or add a holiday gift. The dashboard looks simple, yet its gifting links, contribution tracking, and allocation tool are straightforward.

Where does Utah fit for a Wisconsin family? After you claim Edvest’s $5,280 deduction, my529 suits investors who want to fine-tune risk, tilt toward factors, or chase the lowest sustainable cost without worrying about minimums. Pair the deduction with a custom Utah portfolio and you control taxes and tracking error in one tidy package.

3. Ohio CollegeAdvantage 529: low-cost index funds plus a safety gear

CollegeAdvantage matches Utah and Illinois on price, yet it earns a spot for what Edvest lacks: a true stable-value portfolio. This option credits a bank-style interest rate, protects principal, and lives inside the same tax shelter as your stock funds. When tuition looms and you need to lock gains without moving to cash, that single feature is priceless.

Costs stay slim. Vanguard index tracks land around 0.12 to 0.17 percent, the same neighborhood as Bright Start’s cheapest sleeves. The plan adds no annual account fee and needs just twenty-five dollars to open, so you can park small monthly contributions while your Edvest deduction resets each January.

Morningstar rates Ohio Silver, praising “excellent process and governance” but noting a few pricier active funds. Stick to index or DFA tracks and you avoid that issue. Performance has been steady: the moderate age-based option beat the category median over five and ten years while taking slightly less risk, helped by that conservative cash bucket.

The portal feels familiar if you already invest with Vanguard or Ascensus. Gifting links, payroll direct-deposit forms, and automatic rebalancing sit two clicks deep instead of hiding behind jargon.

How does it fit a Wisconsin plan? Treat CollegeAdvantage like a bond sleeve with extra safety. After you claim Edvest’s $5,280 deduction and load growth dollars into Illinois or Utah, use Ohio to store the slice you cannot afford to see drop 20 percent just before enrollment. It is diversification with purpose, not just another account to monitor.

4. New Hampshire UNIQUE Plan: Fidelity convenience, index costs

Sometimes familiarity wins. If you already use Fidelity for a 401(k) or brokerage account, the UNIQUE 529 appears in the same dashboard. One login, one app, a single view of your net worth. That convenience can improve follow-through: you review balances more often, adjust contributions faster, and stay on track.

You can choose from three tracks— all-index, all-active, or blended. We focus on the index option because expenses stay between 0.11 and 0.18 percent, matching Vanguard’s Nevada plan and sitting just below Edvest’s cheapest sleeve. The funds use Fidelity’s zero-revenue index share classes, so costs are transparent.

Morningstar assigns a Silver medal, praising low fees, a straightforward glide path, and strong parent resources. The trade-off is a smaller menu than Utah or Illinois, but fewer levers mean fewer chances to overthink your mix.

Opening an account is simple. No minimum. Enter the beneficiary’s Social Security number, pick an age-based index portfolio, connect your bank, and you are live in about eight minutes. A gifting page creates a shareable link for birthdays and holidays, and deposits land instantly.

When does UNIQUE fit next to Edvest? Two cases stand out. First, families that keep everything at Fidelity and prefer one portal. Second, parents who like a “set it and walk away” target-date style without chasing the latest fee tweak. Claim your $5,280 Wisconsin deduction in Edvest, then direct extra dollars here and let Fidelity’s quiet efficiency handle the rest.

5. Virginia Invest529: quiet fee cutter with active-optional flair

Virginia rarely lands in headline rankings, yet its direct plan posts some of the lowest expense ratios in the 529 universe. The all-equity index portfolio costs 0.08 percent, and blended tracks that add a touch of active management stay below 0.20. That leaves real distance from Edvest’s 0.31 percent ceiling.

The lineup feels balanced. You get core Vanguard indexes at rock-bottom prices, plus select active managers such as PIMCO on the bond side if you want a bit of professional judgment without hedge-fund fees. Morningstar has shifted the plan between Gold and Silver, consistently praising its state-run governance and habit of trimming costs as assets grow.

Opening an account is easy: ten dollars and an online form. Virginia’s modern dashboard lets you sort funds by enrollment year, static allocation, or single-asset class. Monthly automatic rebalancing keeps your mix on target even if you ignore the account for a while.

For Wisconsin savers the pitch is simple. If you chase every penny of fee savings and find Nevada’s $1,000 minimum frustrating, Virginia delivers nearly the same cost with a pocket-change entry. Layer it on top of your Edvest deduction and perhaps one growth-tilted plan like Utah, and you own a nationally diversified, sub-0.10 percent equity sleeve without sacrificing user experience.

Invest529 is the plan you recommend to friends who ask, “What is the cheapest solid option that is still easy to use?” It offers exactly that—no hype, no hurdles, just efficiency.

6. Nevada Vanguard 529: pure index investing for the Vanguard faithful

If your investing mantra is “own the market and keep costs microscopic,” Nevada’s Vanguard plan feels familiar. Each portfolio relies on the same Total Stock, Total International, and Total Bond index funds you may already hold in an IRA. No style drift, no active surprises, just steady broad-based exposure at 0.12 to 0.16 percent all-in.

That price is about half of Edvest’s highest-cost tracks and only a hair above Illinois’ floor. The trade-off is a $1,000 minimum to open, a by-product of Vanguard’s share-class rules. Families making large lump-sum gifts may shrug at the threshold. New savers adding $100 a month can start elsewhere and move assets after clearing the bar.

Morningstar keeps the plan on its Silver list, citing transparent design and constant fee cuts. There is no flashy mobile app, but the portal mirrors Vanguard’s brokerage interface, so long-time clients feel at home.

Nevada’s edge for Wisconsinites is psychological. Many of us already trust Vanguard with retirement dollars. Holding part of a college fund in the same place reduces mental overhead. Claim the Edvest deduction first, then send windfalls to Nevada. One glance at your Vanguard dashboard shows progress on every goal: retirement, college, everything in one view.

Simplicity, brand trust, and costs near the floor. Sometimes that is all you need.

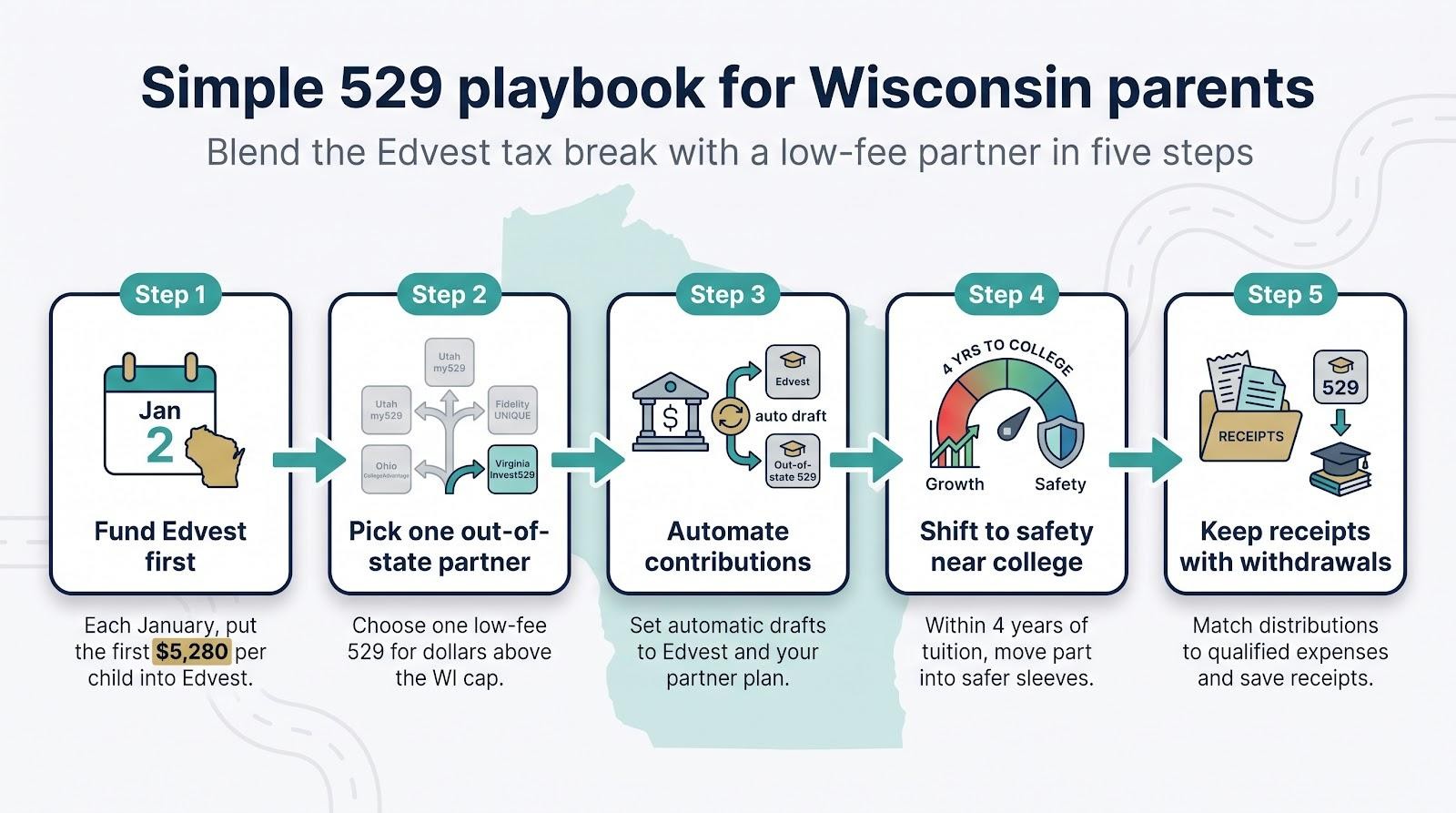

Final tips for Wisconsin parents

Grab the free money first. Set a calendar alert for January 2 and direct the year’s first $5,280 per child into Edvest. That one move can lock in about four hundred dollars of state-tax savings—a risk-free return few investments match.

Next, choose one out-of-state partner that matches your style. Love tinkering? Utah is your playground. Prefer one-click ease? Fidelity’s UNIQUE plan does the job. Need principal protection for a sophomore? Ohio’s stable-value sleeve stands ready. Any of the six plans will pair with Edvest without overlap.

Automate contributions to both accounts on payday. Consistency beats timing, and two automatic drafts take the same effort as one.

Review once a year, not every month. Use tuition age as your guide. When college is less than four years away, move some growth dollars into Ohio’s stable value or Edvest’s principal-plus-interest option and sleep better.

Keep withdrawal records tidy. Match each 529 distribution to a qualified expense in the same calendar year, save digital receipts, and enjoy tax-free growth as Congress intended.

Follow this simple playbook and you will blend Wisconsin’s tax perk with the best features available nationwide, shrinking future tuition bills while keeping your investing life calm.