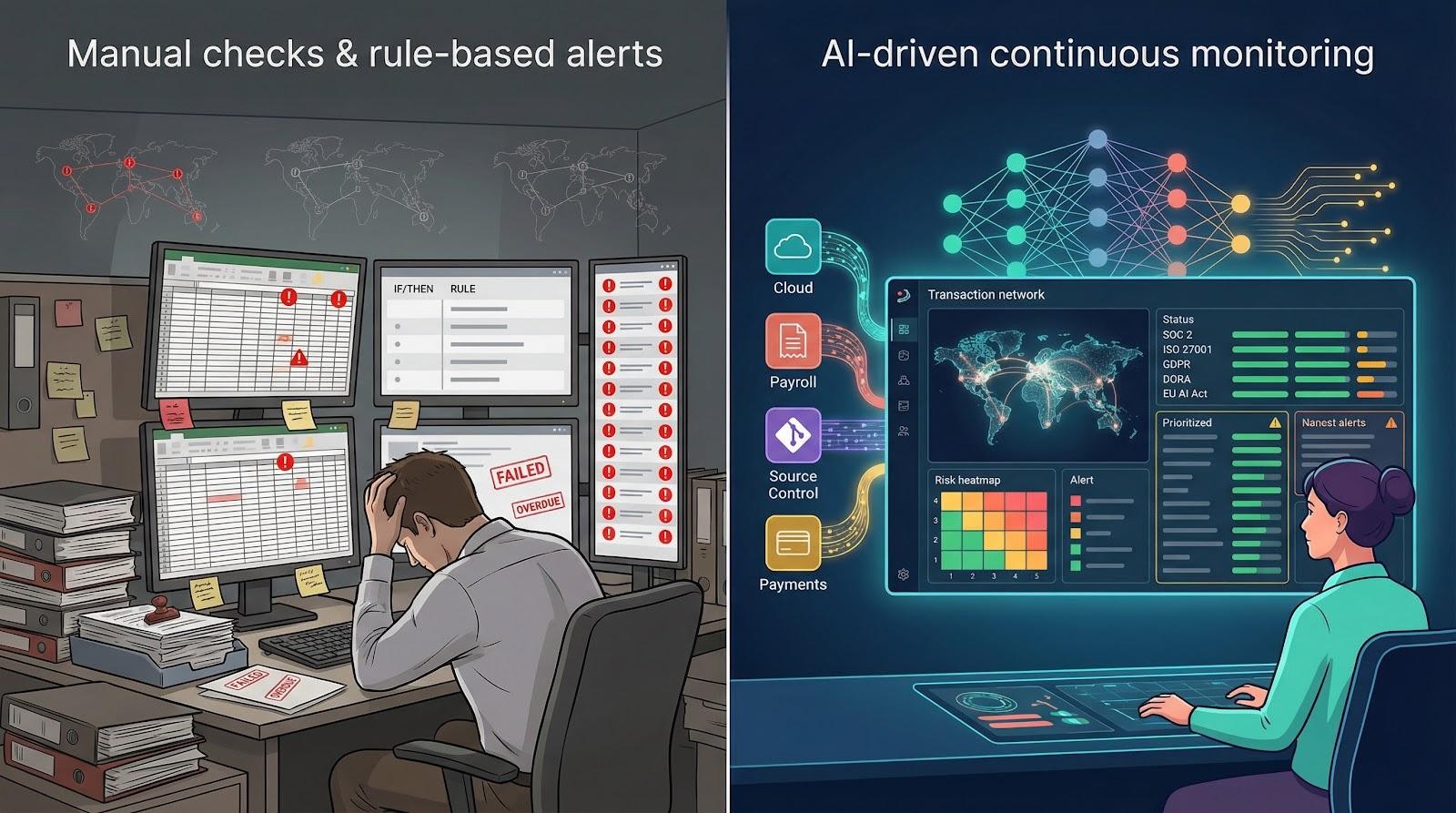

Regulators are turning the screws on fintech. New rules arrive every quarter, security questionnaires land before sales calls, and investors now quiz founders on audit readiness as closely as ARR. Yet the best teams aren’t hiring battalions of compliance analysts; instead, they wire AI-powered compliance platforms into their stack and let the software shoulder the grunt work.

In this guide, we rank four leading AI compliance platforms for fintech. You’ll see how each tool automates evidence, flags risk in real time, and proves to bankers and watchdogs that your house is in order—so you can choose the one that fits best.

How we compared the platforms

Choosing compliance software isn’t as simple as ticking a feature box. We built a scoring model that mirrors the questions you and your auditors ask.

First, we mapped the regulatory pain points shared by neobanks, payments firms, lenders, and crypto exchanges. From there we distilled eight dimensions that separate useful tools from marketing hype: coverage of global frameworks, depth of AI, automation quality, integration breadth, security posture, pricing transparency, market traction, and those small differentiators that turn a demo into a signed contract.

Each dimension carries a weight based on its impact on a fintech: regulatory coverage is worth twenty points, AI and automation earn fifteen points each, integrations receive ten, and the remaining metrics share the last forty. A perfect score is one hundred, but any platform above eighty-five shows it can keep a fast-growing fintech out of hot water.

We reviewed vendor documentation, live product demos, G2 reviews, recent funding rounds, and Reddit war stories where engineers vent about failed audits. Three researchers averaged their scores to reduce bias, then two external compliance consultants checked the outliers.

That process trimmed a longlist of fifteen vendors to the four you’ll meet next. Each cleared the eighty-five bar and offers continuous monitoring, not once-a-year checkbox reports. They serve real fintech customers today, not pilots, and they all use machine learning in ways that save you time rather than add another dashboard to babysit.

1. Vanta – fastest path to an audit-ready trust program

Vanta is a GRC and compliance automation platform built to keep you continuously audit-ready, not just “ready when the auditor asks.” It connects to your existing cloud and SaaS stack, collects evidence automatically, and tests controls on an hourly cadence, so gaps show up while you can still fix them.

Vanta is best for venture-backed fintechs that sell into enterprises, partner with banks, or operate in regulated markets where security reviews and audits sit directly in the revenue path. It tends to fit especially well once you are scaling past the “spreadsheet and screenshots” stage and need a repeatable trust program that holds up across teams, products, and geographies.

What Vanta does well for fintech teams

Once you wire Vanta into your environment, it becomes the system of record for your trust program. You get:

- Broad framework coverage: 35+ pre-built frameworks, including staples like SOC 2 and ISO 27001, plus options like DORA and ISO 42001, with support for custom frameworks when your requirements do not match a standard template.

- Deep integration and continuous evidence: 375 to 400+ native integrations designed for ongoing evidence collection and control testing.

- Buyer-facing trust workflows: A Trust Center for sharing your security posture with prospects and partners without turning every questionnaire into a bespoke project.

- Third-party risk workflows: Vendor Risk Management (VRM) capabilities for handling the reality that your fintech’s risk posture depends on more than your own code.

If you are optimizing for speed, the ROI case is straightforward. IDC research on Vanta users reports teams spend 82 percent less time per framework once the software is live, and adding Vanta risk assessment extends those gains by centralizing the risk register and helping teams remediate issues up to 45 percent faster.

AI that reduces the “compliance busywork” load

Vanta’s AI capabilities are designed to take real work off your team’s plate, especially during audit prep and customer security reviews.

Its AI Agent supports multiple workflows, including control mapping, policy summaries, a policy chatbot, SLA remediation guidance when what you promise does not match what your tests show, evidence evaluation, and bulk policy onboarding. Vanta also applies AI to security questionnaires, with reported performance of roughly 95 percent accuracy and 81 percent faster completion. For customer-facing reviews, Vanta’s Trust Center AI chatbot can help prospects self-serve, with reported results of 87 percent of security reviews being handled without direct back-and-forth.

One practical takeaway for lean fintech teams is that the AI is most valuable when it compresses cycle time. Less time writing narratives and hunting evidence means more time closing deals, shipping product, and fixing real risks.

Pricing and implementation reality check

Vanta pricing varies by headcount, package, and the frameworks and modules you add. Reported starting points for smaller companies begin around $10,500 per year for a basic package with one framework. As you move into growth-stage tiers and larger headcounts, reported annual pricing commonly lands in the $30,000 to $59,000+ range. Additional frameworks are often priced as a flat add-on, commonly cited around $5,000 per year each, and VRM is often treated as an add-on, cited around $7,500 per year. Multi-year discounts are commonly structured around 10 percent for a two-year agreement and 15 percent for a three-year agreement.

On timeline, the platform is built for speed. SOC 2 Type I readiness can be achieved in as little as 4 to 6 weeks, depending on how mature your controls and policies are when you start.

Proof points and differentiators

Vanta’s core differentiator is breadth plus cadence. The combination of 375 to 400+ integrations, hourly monitoring, and 35+ pre-built frameworks is hard to match if your goal is to run a single, continuously updated program across multiple requirements. Vanta also reports 10,000+ customers in 72 countries, and it positions itself as a trust platform, not only an audit checklist tool.

Limitations and where it fits in your stack

Vanta is a strong backbone for security and privacy compliance automation, but it does not replace specialist fintech risk systems.

It is not an AML screening engine, a real-time fraud decisioning platform, a credit underwriting model builder, a financial audit analytics tool, or a model governance system for managing AI risk at the individual model level. In practice, many fintechs pair a platform like Vanta with dedicated tools for AML, fraud, lending model risk, financial assurance, and AI governance.

Bottom line: If your priority is getting audit-ready quickly, staying continuously compliant as you scale, and reducing the operational drag of security reviews, Vanta is one of the strongest “default choices” in the category. It is particularly compelling when compliance is directly tied to revenue velocity, bank partnerships, or enterprise procurement.

2. ComplyAdvantage – real-time AML intelligence without the alert fatigue

ComplyAdvantage is purpose-built for one of fintech’s most expensive failure modes: drowning in AML alerts that do not matter. Instead of treating every partial name match like a fire drill, it combines a continuously refreshed financial crime data set with machine-learning scoring, so analysts spend time on real risk.

Category: AML, KYC, and financial crime compliance

Best for

ComplyAdvantage is a strong fit if your fintech onboards customers, moves money, or supports cross-border activity and you need sanctions screening, PEP checks, adverse media monitoring, and transaction monitoring that can run in real time. It is commonly relevant for payments companies, digital banks, crypto exchanges, and lending platforms with AML obligations.

Core capabilities that matter in practice

At the product level, the platform centers on three jobs your compliance team has to do every day:

- Screening and monitoring: Real-time customer screening at onboarding, plus ongoing monitoring so a previously low-risk customer does not stay invisible when circumstances change.

- Adverse media at scale: Monitoring and parsing adverse media from global sources, not just list checks, so you catch risk signals that show up outside formal watchlists.

- Transaction monitoring and investigations: Transaction monitoring with risk scoring, plus case management workflows for investigations and escalations.

A key element in the pitch is that the underlying data set is proprietary and continuously refreshed. It is not positioned as a simple repackaging of government lists.

AI and why it reduces noise

ComplyAdvantage applies machine learning to score screening hits for relevance, which is what directly attacks false positives. It also uses natural language processing (NLP) to parse adverse media, and it supports an active learning feedback loop where analyst decisions improve model accuracy over time.

The intent is operational, not theoretical: the more your team uses it, the sharper triage becomes.

The result is faster, cleaner decisions with explanations you can take into an audit or an examination without hand-waving.

Regulatory coverage and scope

ComplyAdvantage is aligned to core AML requirements across major jurisdictions, including BSA/AML expectations in the United States, EU Anti-Money Laundering Directives (AMLD 4, 5, and 6), FATF recommendations, and enforcement-oriented regimes and lists such as OFAC, as well as EU, UK, and UN sanctions. It also maps to regulator expectations in markets like Singapore (MAS) and Australia (AUSTRAC).

It is important to separate this from security compliance. This tool does not replace SOC 2 or ISO 27001 automation.

Integrations, pricing, and rollout expectations

ComplyAdvantage is API-first. You embed it where risk decisions actually happen, including signup flows, payment processing, and batch back-office checks. That makes it easier to adopt without redesigning your stack.

Pricing is volume-based, typically structured as a platform fee plus per-screen or per-transaction costs. Basic screening can be integrated relatively quickly, often in days to weeks. Full transaction monitoring deployments usually take longer because they require tuning to your products and risk appetite.

Proof point, limitations, and fit

The clearest performance claim in the draft is the operational outcome: FinTech Magazine reports customers see false positives drop by 70 percent, which is the difference between a queue your team can clear and a queue that grows forever.

The limitation is scope. ComplyAdvantage is not a full GRC suite. It does not manage SOC 2, ISO 27001, HIPAA, or general IT controls, and it is not a real-time fraud decisioning platform.

Bottom line: If your question is “are we screening and monitoring customers and transactions in real time, with fewer false positives,” ComplyAdvantage is built for that. Most fintechs pair it with a GRC platform like Vanta for audit readiness, and with a fraud platform like Feedzai when they also need millisecond transaction fraud prevention.

3. Feedzai – fraud defense at millisecond speed

Feedzai is an enterprise fraud and financial crime prevention platform built for one job: make a decision on every event fast enough that customers never notice the risk you just blocked. It is AI-native and designed to operate at payment-switch scale. Feedzai positions its footprint in hard terms, including protecting $9 trillion in payments annually.

Category: Fraud detection and financial crime prevention (RiskOps)

Best for

Feedzai is a strong fit for fintechs and banks once transaction volumes are high enough that fraud becomes a balance-sheet line item. Think cards, real-time payments, P2P, and high-velocity account activity where you need to score risk in real time and still keep approval rates healthy.

It is not built as a self-serve tool for early-stage startups. Most teams evaluate Feedzai when they have enough history and volume to justify a full decisioning layer.

What you get in the platform

Feedzai’s RiskOps platform spans multiple fraud and fincrime surfaces, including:

- Identity: account opening fraud signals, behavioral biometrics, and device intelligence

- Fraud: real-time transaction scoring across channels, including scam and authorized push payment style threats

- AML: screening and transaction monitoring capabilities, plus workflows that support investigations

A practical differentiator is consolidation. Instead of running separate point tools with separate queues, Feedzai ties signals together with a unified case manager and behavioral profiles that can help teams understand the “shape” of activity for a given customer or network.

AI and explainability

Feedzai’s pitch is not just that it uses machine learning. It is that machine learning is the foundation, and the decisions remain explainable. The platform supports pre-trained models for day-one performance and AutoML-driven retraining. It also introduced RiskFM, described as a tabular foundation model built specifically for financial transaction data.

For regulated environments, the explainability layer matters as much as the model. Feedzai provides human-readable decision outputs, including plain-text reason codes. It also points to responsible AI work, including open-sourced fairness tooling such as TimeSHAP, FairGBM, Fairband, and Aequitas.

Integrations and operational realities

Feedzai is delivered as a cloud-native REST API service for real-time decisioning. It reports average latency around 20 ms, while noting that teams should evaluate tail latency (p99) as part of production readiness. At scale, it can process 3,000+ events per second.

It also works in the ecosystem where banks and larger processors live, including partnerships such as Jack Henry, which reaches 1,000+ U.S. financial institutions, along with integrations and partnerships referenced with providers like Fiserv and Shift4.

Implementation is not instant. Feedzai deployments typically require historical data loading, defining risk appetite, and tuning models and workflows to your channels and products. This is the trade-off for industrial-grade performance.

Security posture (vendor assurances)

Feedzai notes vendor-side security and compliance credentials including PCI DSS Level 1, ISO/IEC 27001, SOC 2, and GDPR. These are useful for vendor risk reviews. They do not replace your own compliance program.

Pricing and timeline

Feedzai is enterprise-only with custom pricing. The expert research notes estimates that commonly fall in the $500K to $5M+ range for enterprise deployments, depending on scale and scope.

Proof points and differentiators

Feedzai operates at a large scale, including 1 billion+ consumers, $9 trillion in payments, and 120 billion events annually. It also publishes customer outcomes, for example Elo reporting a 90 percent fraud reduction, along with other results across banks and processors.

Key differentiator: Feedzai combines identity, fraud, and AML capabilities into a single RiskOps system, adds foundation-model work tailored to tabular financial data, and keeps explainability front and center for regulated use cases.

Limitations and how it fits your stack

Feedzai is not a GRC platform. It will not help you achieve SOC 2 or ISO 27001 by automating cloud controls, policies, or audit workflows. It is also not priced or packaged for lightweight adoption, and it typically demands meaningful data and operational investment to deploy well.

Complements well with: Vanta or Drata for audit readiness and security compliance automation, and ComplyAdvantage if you want additional depth in sanctions, PEP, and adverse media screening beyond a fraud-first system.

Bottom line: If you authorize money movement at scale and need real-time decisions that stand up to scrutiny, Feedzai is built for that tier. Just go in expecting enterprise implementation and enterprise economics.

4. Lumenova AI – governance armor for the EU AI Act playbook

Most fintech teams have matured their security compliance programs. Model governance is usually still a spreadsheet. That gap is about to get expensive.

Under the EU AI Act, credit scoring is treated as a “high-risk” system. The law also introduces meaningful penalties, including fines up to three percent of global revenue for non-compliance and up to seven percent for prohibited practices. In the U.S., model risk expectations often get routed through SR 11-7, and examiners increasingly expect audit-ready evidence.

Lumenova AI is built to close that model-governance gap. The simplest way to understand it is the analogy from earlier. It is “Vanta for algorithms.”

Category: AI governance and model risk management

Best for

Lumenova AI is best for fintechs that deploy AI in regulated decisions, including underwriting, credit models, and risk systems, and need to demonstrate governance against frameworks like the EU AI Act, NIST AI RMF, and ISO/IEC 42001. It is also relevant when SR 11-7 style model risk management documentation is becoming a standard partner or regulator task.

One important caveat affects fit. Lumenova is an early-stage company, founded in 2022 with roughly 20 employees. You should evaluate that maturity and vendor risk profile as part of the decision.

What the platform does

Lumenova’s core workflow is about making your AI systems legible to outsiders and manageable internally.

It provides:

- AI inventory: A centralized registry of AI systems, including model-card style documentation.

- Evaluations and assessments: An evaluation engine with 200+ metrics across eight risk verticals, including fairness, explainability, validity and reliability, security and resilience, data integrity, hallucination detection, monitoring, and observability.

- GenAI guardrails: Governance features designed for GenAI use cases, including hallucination detection and prompt and output governance.

- Lifecycle governance: Support for gating and approvals across development, validation, deployment, and monitoring.

- Collaboration workflows: Review chains, threaded comments, and approval gates that keep legal, compliance, and data science aligned.

Where this becomes practical is in packaging evidence. Lumenova is designed to generate audit-ready evidence packs that bring together what regulators and partners typically request, without forcing your team to reconstruct the narrative from tickets, notebooks, and half-finished docs.

AI capabilities

Lumenova’s “AI” is less about generating text and more about evaluating and monitoring models. It emphasizes quantitative and qualitative assessment across a broad set of metrics, plus ongoing checks for drift, bias, outliers, and data quality issues. For explainability, it supports SHAP or LIME style tracing. For GenAI, it focuses on hallucination detection and governance controls.

Frameworks and regulations covered

Lumenova maps work to multiple frameworks and regimes, including:

- EU AI Act

- NIST AI RMF

- ISO/IEC 42001

- SR 11-7

- Colorado SB 24-205 (algorithmic discrimination)

This scope is model governance. It does not replace a SOC 2 or ISO 27001 program.

Integrations and implementation reality

Lumenova is positioned as a central governance layer. However, third-party analysis rates both API extensibility and ML platform integrations as “Basic.” It also notes the platform does not auto-discover models from ML pipelines, which means model onboarding can require more manual cataloging than some enterprise-first alternatives.

Deployment options include SaaS and single-tenant cloud. There is no on-premises or air-gapped deployment option called out in the expert research.

Lumenova also offers a Forward Deploy Team, which signals hands-on implementation support. The company does not publicly specify a standard implementation timeline. In practice, time-to-value will depend on how many models you need to onboard and how standardized your current ML tooling is.

Pricing

Pricing is not listed publicly, but the expert research includes third-party tier estimates:

- Startup and SMB (up to 25 models): $25,000 to $45,000 per year

- Mid-market (25 to 100 models): $50,000 to $100,000 per year

- Enterprise (100 to 500 models): $120,000 to $250,000 per year

- Large enterprise (500+ models): custom

Notably, implementation support, a dedicated CSM, training, and compliance template updates are included at all tiers in these estimates. Custom integrations are extra.

Proof points and buying risk

This is where buyers should be extra disciplined. The expert research flags a significant validation gap.

Lumenova has no named customers publicly available, no G2 profile or reviews found, and only one published case study presented as an illustrative scenario for a retail bank rather than a named customer. That does not mean the product is ineffective. It does mean you should run a thorough pilot and treat vendor maturity as a first-class requirement.

Key differentiator and limitations

Key differentiator: An accessible entry price point for AI governance, a UX that non-technical stakeholders can use, and dedicated customer support across tiers.

Limitations: Early-stage maturity and lack of public customer references. “Basic” integration and extensibility ratings from third-party analysis. No on-prem deployment option. Monitoring is described as more dashboard-oriented, without automated alerting called out in the expert research. Bias testing is also rated as narrower than some competitors, with eight bias metrics cited versus 15+ for Holistic AI.

Bottom line

If you have AI systems that will be scrutinized under the EU AI Act or SR 11-7 style model risk expectations, Lumenova covers a governance layer that traditional GRC tools do not. Just be explicit about the trade-off. You are getting an approachable, governance-first platform, but you are also taking on more vendor maturity risk than you would with the larger, more established platforms in this list.

Side-by-side snapshot

You have met the players; here is the cheat sheet. Scan the grid, spot the gaps, and shortlist the two or three platforms that align with your biggest pain point. We focus on the factors that shape budgets: framework coverage, AI depth, automation power, integration reach, security signals, typical pricing, and ideal use case.

| Platform | Framework breadth | Signature AI capability | Continuous automation | Integration depth | Security creds | Price band* | Best for |

| Vanta | 35+ pre-built frameworks, plus custom | AI Agent workflows plus questionnaire automation | Hourly control testing and evidence collection | 375 to 400+ native integrations across cloud and SaaS | SOC 2 Type II, ISO 27001 | $$ | Fast-growing SaaS and fintechs needing audit readiness |

| ComplyAdvantage | Global AML/KYC rules | ML risk scoring plus NLP adverse media | Real-time screening and monitoring | API embeds in onboarding and payments | ISO 27001 | $–$$ | Payments, crypto, and digital banks fighting fincrime |

| Feedzai | PSD2, FFIEC fraud guidance | Deep-learning risk scores with explainability | Millisecond transaction scoring | API at payment-switch scale | ISO 27001 | $$ | High-volume processors needing top-tier fraud defence |

| Lumenova | EU AI Act, NIST AI RMF, ISO 42001 | AI inventory plus risk assessments | Model lifecycle monitoring | Hooks to MLflow, SageMaker, Jira | Role-based, encrypted | $–$$ | AI-heavy fintechs preparing for upcoming AI regulations |

*Price symbols: $ mid-five-figure annual, $$ low-six-figure annual, $$$ higher-six-figure annual.

Use the grid as a reality check: if your core risk is sanctions screening, Vanta’s scoring focus will not help; if the EU AI Act looms, place Lumenova at the front.

Next steps and final thoughts

Compliance once followed product launches; today it decides who wins contracts, secures bank partnerships, and opens new markets. The four platforms you just explored prove that automation and AI now drive the playbook.

Line up a trial. Give the vendor access to a sandbox environment and track three numbers:

- Hours of manual evidence or alert review eliminated.

- Time from “we need this framework” to auditor sign-off or regulatory approval.

- Deals won or fraud losses avoided because you answered risk questions on the spot.

If the pilot fails to improve at least one metric, switch providers. The market offers real choice, and inertia is the only penalty.

Remember: buying a tool is the start, not the finish. Assign owners, wire integrations on day one, and schedule regular health checks. A compliance platform that runs quietly in the background is the closest thing fintech gets to peace of mind.

Emerging trends and buyer FAQs

What new rules will shape roadmaps in 2026?

The EU AI Act tops every vendor backlog. Platforms from Vanta to Lumenova now map controls to the final draft text and log model-level impact assessments. In parallel, Europe’s DORA resilience regime pushes GRC tools to monitor cloud downtime and third-party risks continuously rather than quarterly. Expect U.S. regulators to borrow language; the Fed’s SR 11-7 guidance already serves as a catch-all for AI governance reviews.

Will large language models replace checklists?

LLMs already draft policies, classify evidence, and answer security questionnaires. Vendors keep the models on short leashes: generative text is gated behind human review to avoid hallucinated controls. Augmentation, not autonomy, wins the day; your analysts stay in the loop, and the inbox grind disappears.

How do I justify budget to the board?

Point to three hard numbers: audit prep hours cut, deals closed faster, and risk events prevented. Vanta users report spending 82 percent less time per framework, while banks running Feedzai cut fraud losses yet keep approval rates high. Translate each metric into revenue or headcount savings, and the ROI speaks for itself.

Can a single platform really cover every framework?

Not today. Broad suites automate infosec controls; niche tools excel at AML, fraud, or AI governance. Most high-growth fintechs run a two- or three-tool stack: one for cloud and privacy attestations, one for financial crime, and, increasingly, one for model risk. Integration APIs keep the mix manageable.

When should a startup buy versus build?

Buy early if a bank partner or regulator sits in the critical path—speed to proof beats perfection. Build in-house only when you hold a specialised risk model that delivers competitive advantage and have the team to maintain validation packages. Even then, platforms like Lumenova wrap governance around bespoke code.