A lease buyout rate is the cost of keeping a leased asset instead of handing it back. Simple idea, bigger consequences. Lease buyout rates 2026 are important because financing still costs real money, used-equipment prices aren’t moving in one clean direction, and lenders are asking tougher questions.

For business owners, the old habit of assuming a buyout is the easy next step doesn’t hold up as well this year. You have to compare three doors, buy, renew, or return, and each one hits cash flow, uptime, and future flexibility in a different way.

The market feels calmer than the last few years, but calmer doesn’t mean cheaper. It means the details matter again, and that starts with knowing what sits inside the buyout price.

What lease buyout rates mean for business owners in 2026

A lease buyout lets you purchase equipment, vehicles, or other business assets at the end of a lease. The final number isn’t only the unpaid balance. It can include the contract’s purchase formula, the asset’s residual value, current market value, fees, and the rate on any money you borrow to fund the deal.

How to Buyout Your Car Lease [EXPLAINED]

2026 feels different because the capital market is cooler and more predictable than it was during the whiplash years. The average amount financed is $31,866 as of June this year.

Still, money isn’t cheap. Used-asset pricing is steadier in some categories and messy in others. Some lessors also want liquidity, which can open the door to better terms, but they still price risk carefully.

Why higher interest rates can push buyout costs up

If you finance the buyout, the interest rate changes the whole picture. A one-point difference on a six-figure machine can add thousands over the loan. That matters when you’re choosing between keeping a familiar asset, taking a new lease, or paying cash.

New equipment loans can also come with different terms than lease-end buyout financing. So the right question isn’t, “Can I handle this payment?” It’s, “What does ownership cost over the full term?”

How residual value affects the final buyout number

Residual value is the lender’s estimate of the asset’s value at the end of the lease. If that estimate is high, the buyout can feel expensive. If it’s low, keeping the asset may be a bargain.

Lenders watch residuals more closely in 2026 because some assets age faster now. Equipment tied to software, automation, or AI upgrades can lose value more quickly than expected. Older assets with weak resale demand can also get tougher pricing at lease end.

Which assets make the smartest buyout candidates this year

Not every leased asset deserves a permanent spot on your books. The smartest buyout candidates are usually the ones you know well, use often, and can keep productive for years without ugly repair surprises.

Equipment with strong resale value and long useful life

Think about assets with stable secondhand demand and long service lives, such as heavy equipment, trailers, generators, or durable production machines. If the asset still performs well and parts are easy to get, a buyout often makes sense.

There’s another advantage here. You already know the maintenance history, operator habits, and weak spots. That lowers the risk of buying a problem you haven’t seen yet.

Assets tied to fast-changing tech and AI

Some equipment ages like cast iron. Some ages like a phone. That’s the split that matters in 2026.

If software updates, sensor packages, AI features, or integration requirements drive the value, ownership gets riskier. Servers, specialized imaging systems, smart warehouse gear, and tech-heavy office equipment can fall behind fast. A manageable payment can hide the fact that the asset may be outdated before the loan is done.

When the value lives in the software, old hardware can get expensive in a hurry.

How lease buyout rates could shape your acquisition strategy

A lease-end choice isn’t a side decision. It affects capital spending, borrowing room, and how much cash you keep for payroll, inventory, or growth.

When buying out can beat replacing equipment

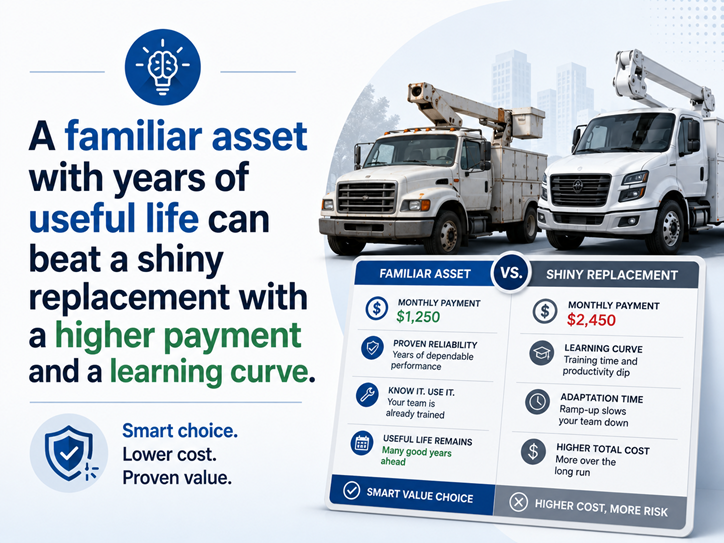

A buyout often wins when the asset is core to operations, downtime would be expensive, and the current unit still has solid years left. You avoid the disruption of installation, training, and workflow changes. You also keep a machine or vehicle with a performance record you already trust.

This can look even better when new equipment pricing stays high. If the buyout price sits below the current market value, the math can tilt toward ownership fast. Stable financing conditions help, but the bigger win is often continuity. No restart, no surprises, no lost hours while a new asset gets up to speed.

When it may be better to walk away and lease again

Sometimes the smartest move is to hand the keys back. Rising repair bills, falling usage, or a shift in production needs can wreck the case for a buyout, especially with equipment or company cars that no longer match daily operations. So can a model that’s becoming hard to support.

A cautious 2026 market also makes flexible lease structures more appealing. If your needs may change in a year or two, a fresh lease can protect cash and keep your upgrade options open. Some lessors are also more willing to discuss creative renewal terms when they want assets placed quickly.